What does the home buying and selling process look like in the nuanced, fast-paced Los Angeles market?

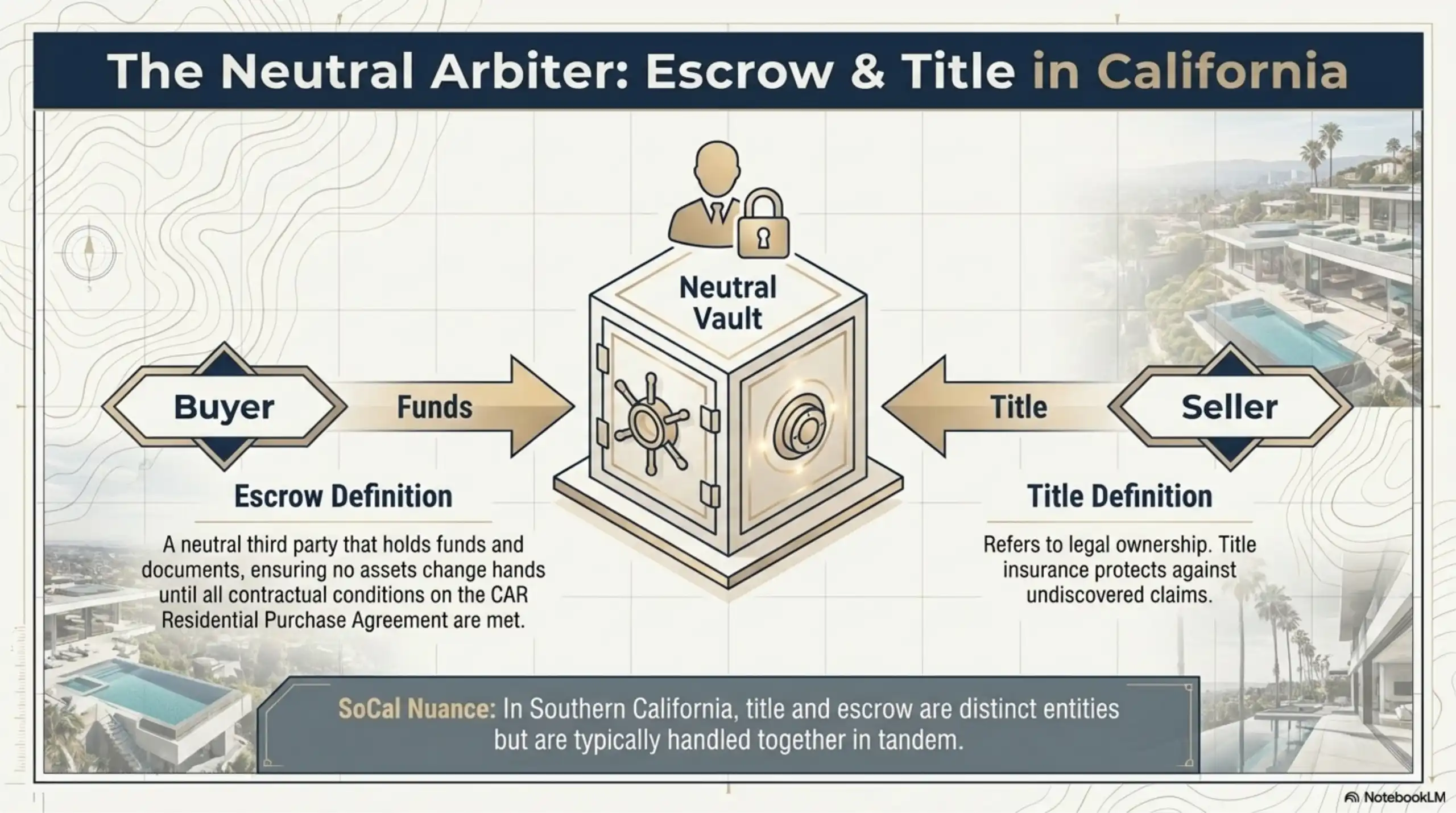

In California, real estate transactions run through escrow — a neutral third party that holds funds and documents until all contractual conditions are met. From the moment an offer is accepted to the day keys are handed over, the process typically takes 30 to 45 days in Los Angeles. However, in our current 2026 landscape, characterized by fluctuating interest rates and distinct neighborhood inventory shortages, timelines can shift rapidly based on financing, inspections, and strategic negotiations.

Most people searching “how does escrow work in California” or “what is a contingency in real estate” find generic, national content that skips California’s stringent requirements. They miss the crucial local nuances—like Los Angeles transfer tax structures (including Measure ULA), complex Natural Hazard Disclosures, and hillside ordinance compliance.

Source: For foundational data on statewide housing guidelines and contract standards, we reference the California Association of REALTORS® (C.A.R.) Market Data.

Whether you’re buying your first architectural home in Silver Lake or selling a longtime family estate in Sherman Oaks, here is exactly what you can expect, step by step.

FAST FACTS: LA Real Estate Process at a Glance

- Average Escrow Length: 30 to 45 days (often condensed to 21 days for cash or highly qualified buyers).

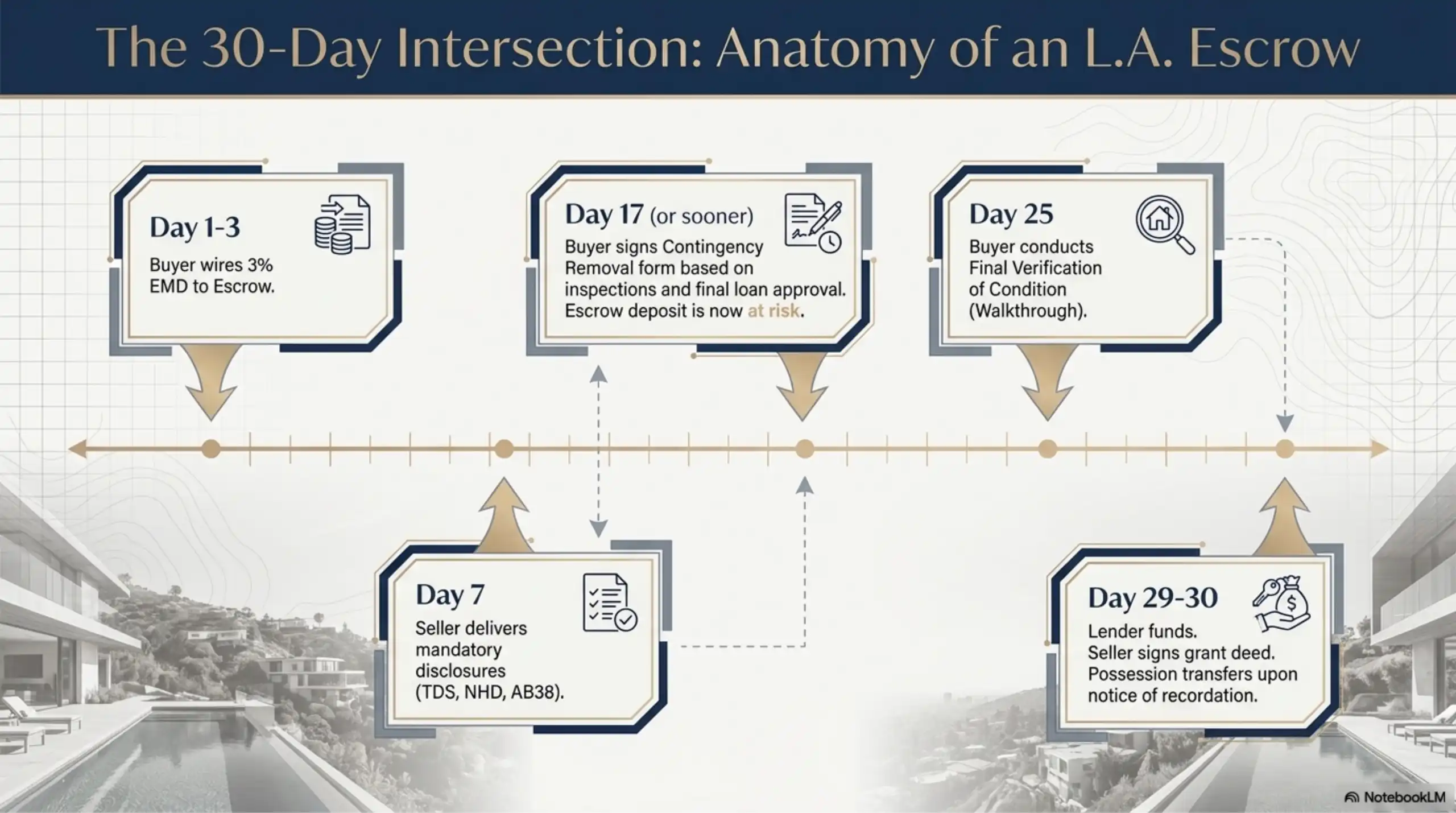

- Standard Earnest Money Deposit (EMD): 3% of the purchase price, due within 3 business days of acceptance.

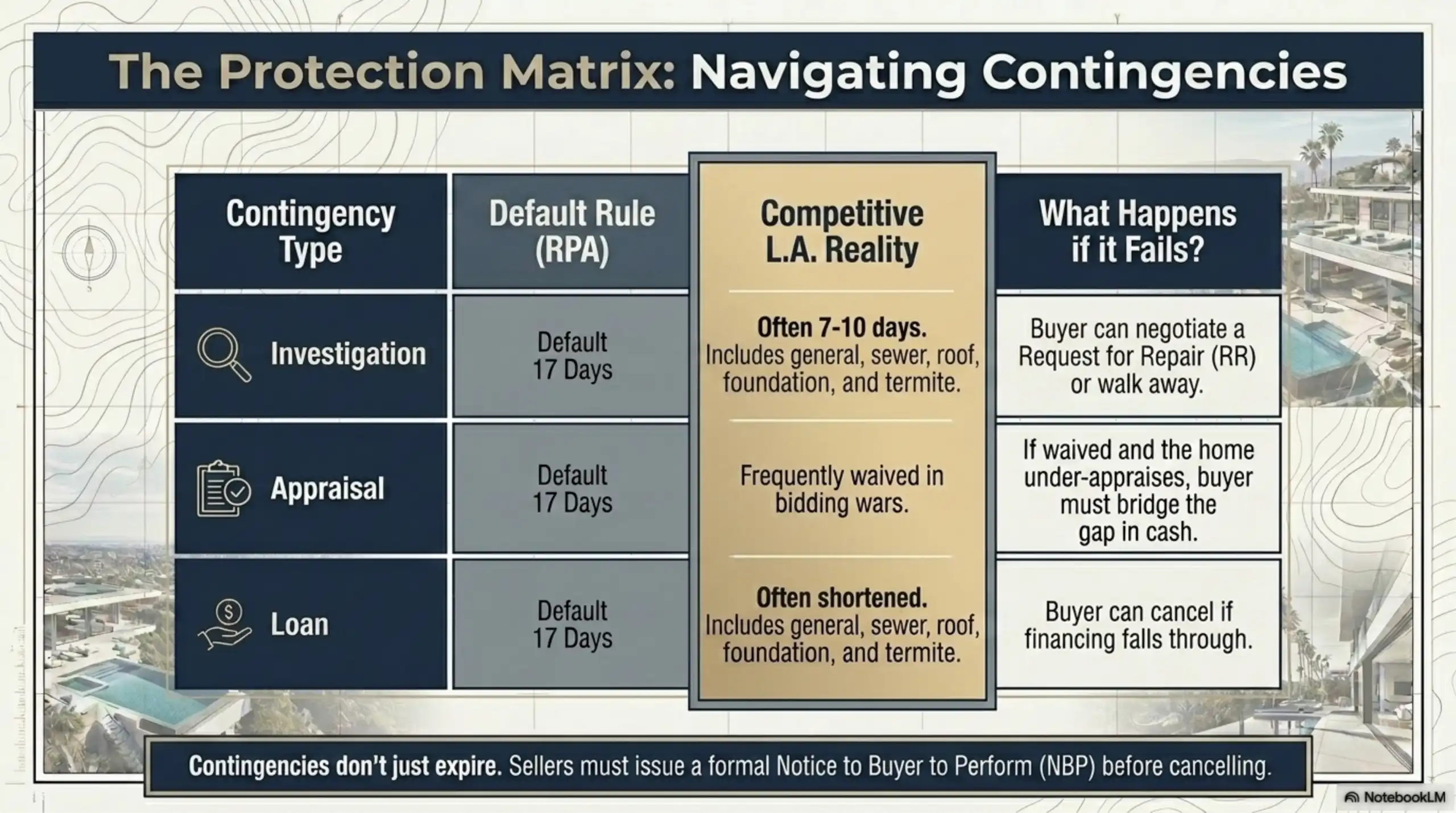

- Default Contingency Periods: 17 days for Loan, Appraisal, and Investigation (often negotiated shorter in competitive LA neighborhoods).

- LA Specifics: Sellers must navigate strict local disclosures, including high-fire hazard retrofitting (AB 38) and city-specific transfer taxes.

Navigating the 2026 Los Angeles Market: Inventory and Interest Rate Impacts

Before diving into the steps, it is vital to understand how the current market environment dictates contract terms. Los Angeles continues to experience pockets of tight inventory, particularly in highly desirable enclaves like Brentwood, Studio City, and Mar Vista.

When inventory is constrained, buyers must write aggressive offers to win. This often means shortening contingency periods from the default 17 days down to 10 or even 7 days to appeal to sellers. Furthermore, with the ongoing stabilization of interest rates in 2026, lending guidelines remain rigorous. A slight fluctuation in interest rates during your escrow period can impact your debt-to-income ratio, making strict adherence to your loan contingency timeline absolutely critical.

Part One: The Buyer’s Process

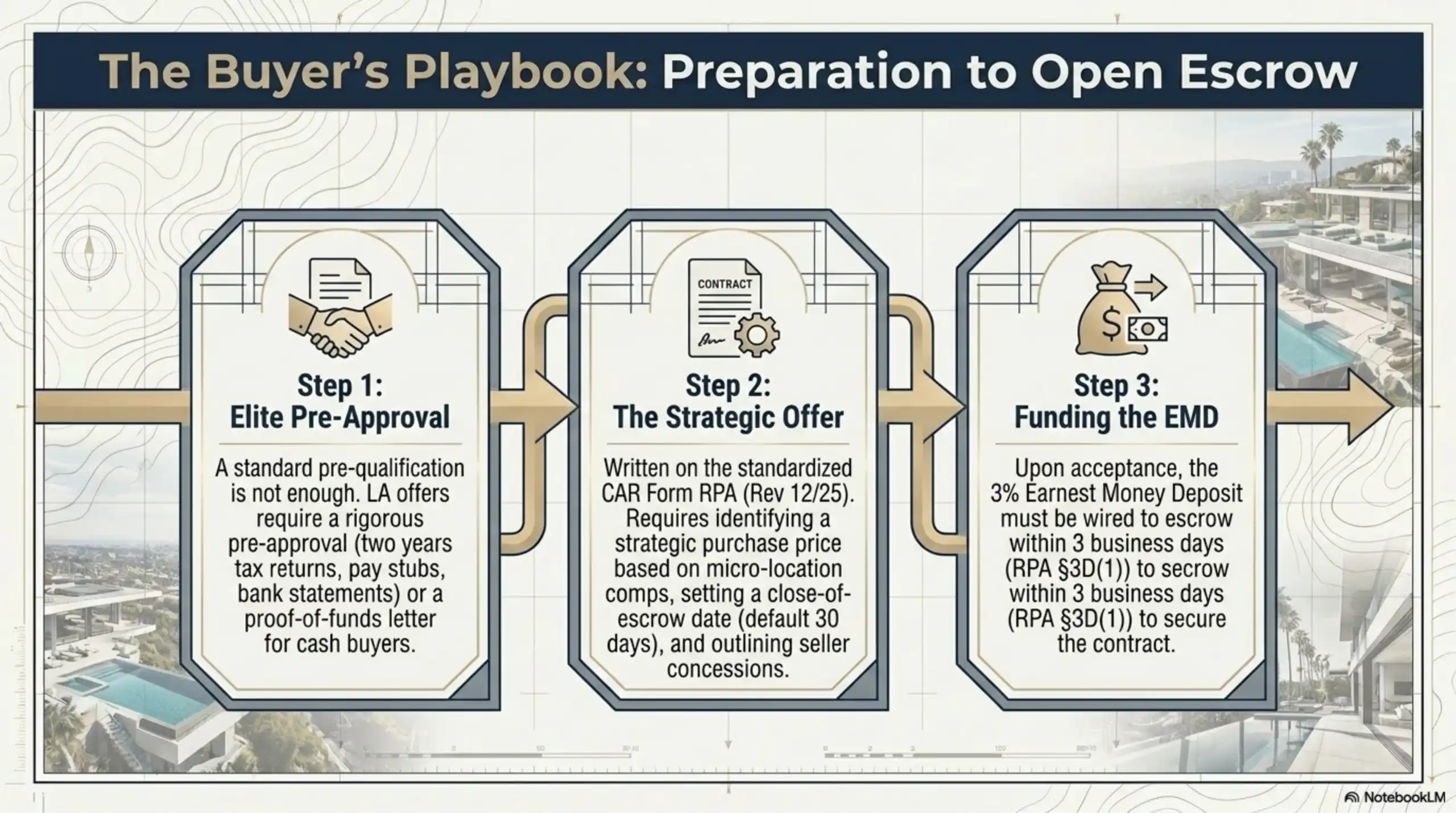

Step 1: Get Pre-Approved (Before You Shop)

Pre-approval is not the same as pre-qualification. In a competitive Los Angeles market, a pre-approval letter from a lender who has thoroughly reviewed your income, assets, and credit is required just to have your offer considered.

Plan to gather: two years of tax returns, recent pay stubs, bank statements, and a list of monthly debt obligations. Your lender will pull your credit and issue a letter. If you are paying cash, you will provide a proof-of-funds letter instead. A strong pre-approval—ideally from a reputable, local lender who understands LA property types—signals you’re serious and capable of closing.

Step 2: Find the Right Home and Make an Offer

Once we identify a property, we will pull comparative sales (comps) to determine a strategic offer price. Your offer will include:

- Purchase price

- Earnest money deposit (3% of the purchase price, wired within 3 business days of acceptance per RPA §3D(1))

- Contingency periods

- Proposed close-of-escrow date (default is 30 days — RPA §3A)

- Any requested seller concessions

California offers are written on the CAR Residential Purchase Agreement (CAR Form RPA, Revised 12/25), a standardized contract that defines your rights.

Step 3: Understand Your Contingencies

Contingencies are protective clauses allowing you to cancel the contract—and recover your deposit—if specific conditions aren’t met.

1. Loan Contingency (default: 17 days — RPA §3L(1) / §8A)

This protects you if your financing falls through. Note: if there is no appraisal contingency, a low appraisal does not automatically entitle you to cancel under the loan contingency.

2. Appraisal Contingency (default: 17 days — RPA §3L(2) / §8B)

If the home appraises below the purchase price, you can renegotiate, make up the difference in cash, or cancel. Removing the loan contingency does not automatically remove the appraisal contingency. Waiving this is common in LA bidding wars, but carries real financial risk.

3. Investigation of Property Contingency (default: 17 days — RPA §3L(3) / §8C)

This allows you to inspect the property and approve its condition, negotiate repairs, or walk away. In tight LA markets, buyers frequently shorten this window.

Contingencies do not simply vanish when the clock runs out. The seller must serve a Notice to Buyer to Perform (CAR Form NBP) before exercising any cancellation rights.

Step 4: Open Escrow and Complete Due Diligence

Once accepted, escrow opens. A neutral title and escrow firm holds your deposit and coordinates the transaction. During this 17-day window, you will:

- Complete inspections (such as: general, sewer, roof, foundation, pool & chimney).

- Deliver written verification of your down payment and loan application (within 3 days).

- Review seller disclosures (Transfer Disclosure Statement, Natural Hazard Disclosure).

- Finalize your loan and appraisal.

- Review the preliminary title report.

Step 5: Remove Contingencies and Head to Close

Once you are satisfied with your inspections, disclosures, and loan approval, you will sign a Contingency Removal form. At this point, your earnest money deposit is at risk if you back out without a valid contractual reason.

In the final days, you will complete a Final Verification of Condition (walkthrough), receive a Closing Disclosure from your lender, sign loan documents with a notary, and wire your final funds. Possession transfers upon notice of recordation (RPA §M(1)), typically the same or next business day after the lender funds.

Part Two: The Seller’s Process

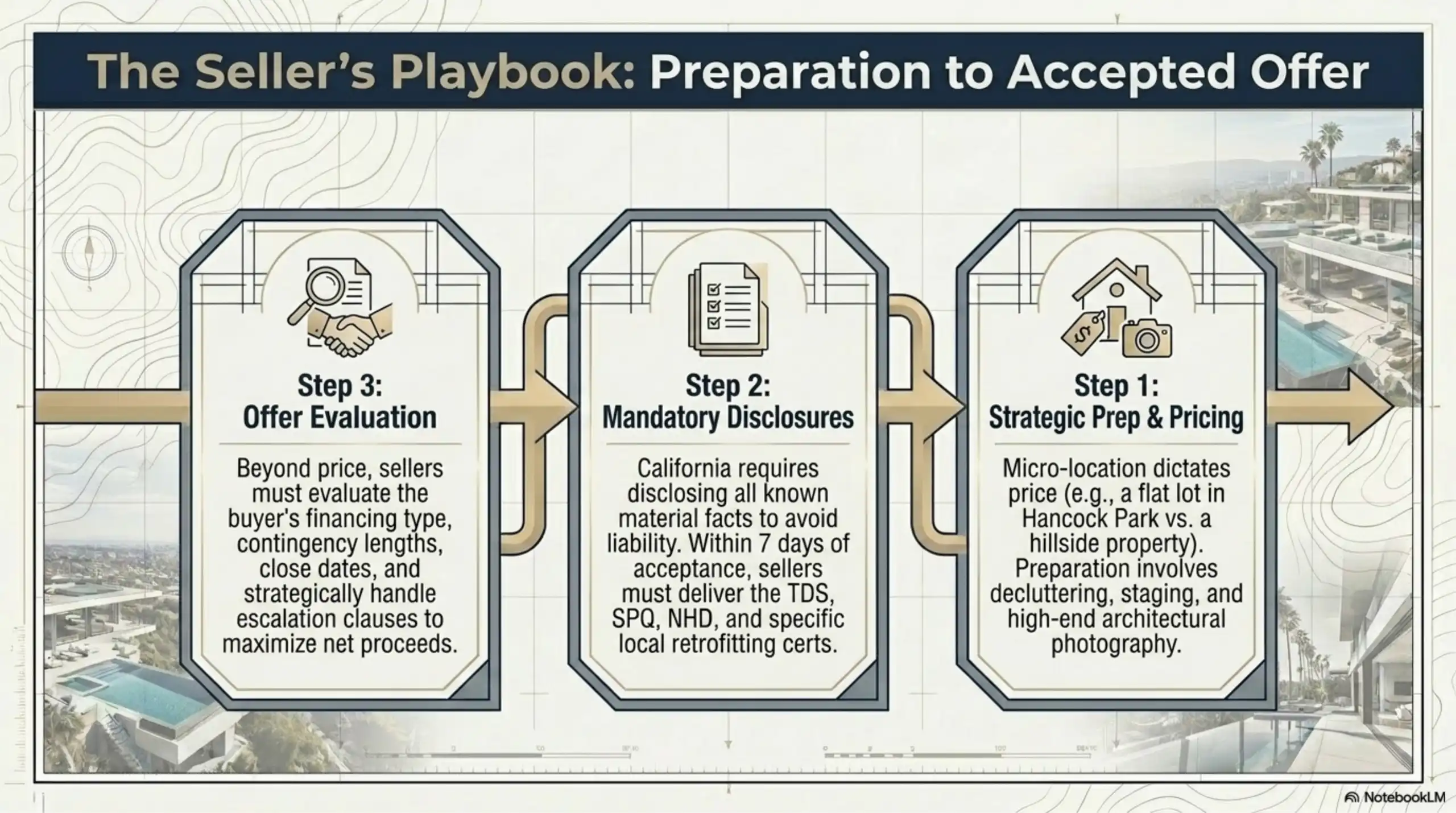

Step 1: Prepare Your Home and Set the Right Price

Pricing is your most consequential decision. Price strategically, and you generate multiple offers. In Los Angeles, micro-location matters enormously; a flat lot in Hancock Park prices entirely differently than a hillside property in the same ZIP code.

Before listing, we will focus on decluttering, light cosmetic repairs, professional staging, and high-end architectural photography.

Step 2: Complete Your Seller Disclosures

California sellers must disclose all known material facts to avoid future legal liability. Key documents (due within 7 days of acceptance) include:

- Transfer Disclosure Statement (TDS)

- Seller Property Questionnaire (SPQ)

- Natural Hazard Disclosure (NHD)

- Seismic safety and water heater bracing certifications

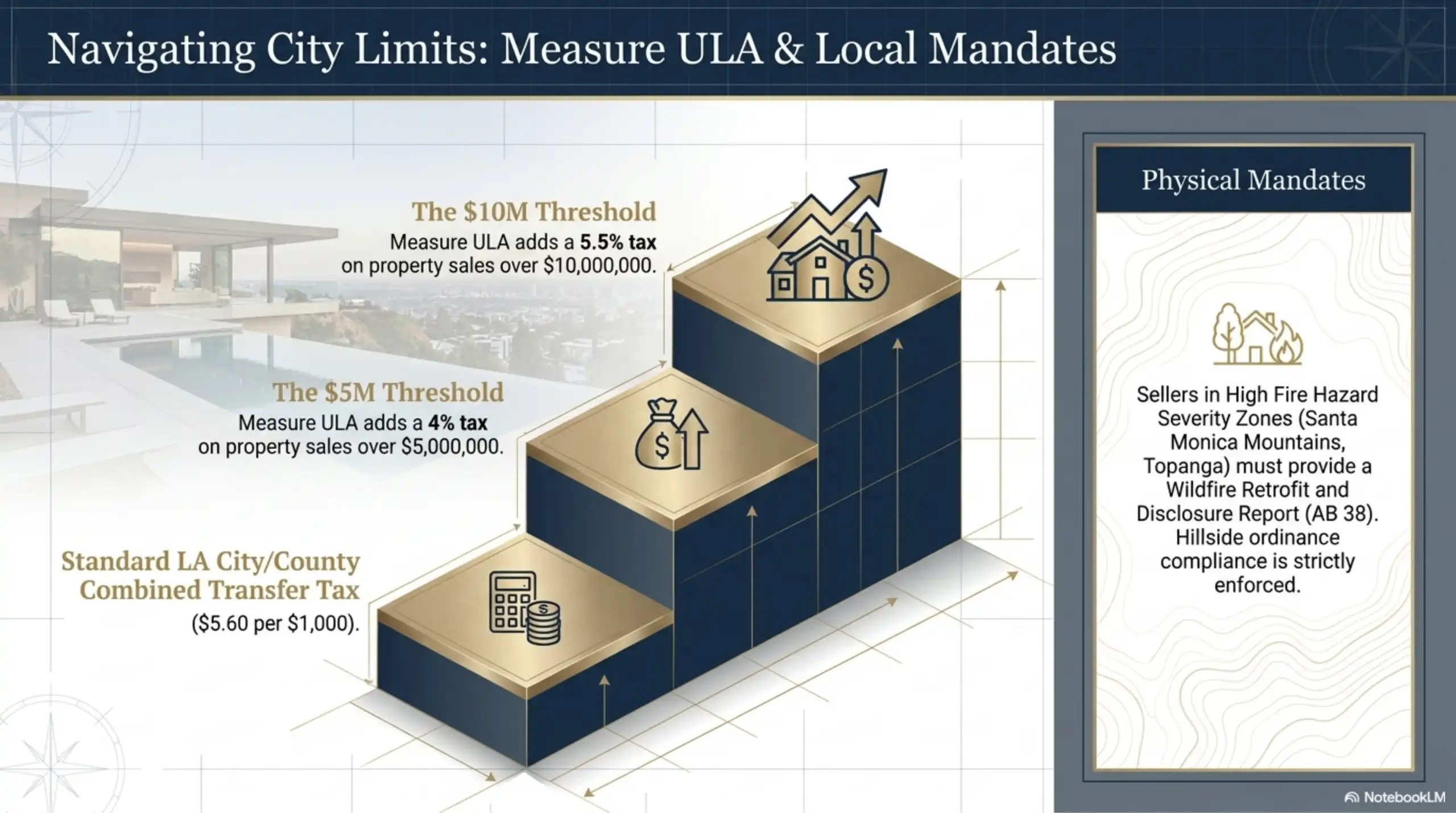

For properties in High Fire Hazard Severity Zones (like the Santa Monica Mountains or Topanga), sellers may be required to provide a Wildfire Retrofit and Disclosure Report under AB 38.

Step 3: Go to Market and Review Offers

When reviewing offers, price is just one factor. We evaluate financing type, contingency terms, close dates, and earnest money deposits. In our low-inventory market, you may receive escalation clauses, which require strategic handling to maximize your net proceeds without alienating buyers.

Step 4: Open Escrow and Navigate the Inspection Period

During the buyer’s contingency window, expect inspections and a potential Request for Repair (CAR Form RR). You can agree, counter, or decline. If the buyer cancels after contingencies are removed, you may have a claim to their deposit, provided both parties initialed the Liquidated Damages clause (RPA §29).

Step 5: Close Escrow and Transfer Title

You will sign a grant deed, settlement statement, and certifications. Seller closing costs include commissions, escrow/title fees, prorated taxes, and transfer taxes.

Note on Transfer Taxes: In the City of Los Angeles, base transfer tax is $4.50 per $1,000 (plus LA County’s $1.10). Additionally, Measure ULA imposes a 4% tax on sales over $5,000,000 and 5.5% on sales over $10,000,000.

The Full Timeline at a Glance

(Based on CAR Form RPA, Revised 12/25. Days are calendar days from acceptance.)

| Milestone | RPA Reference | Default Timeline |

| Offer expires if not accepted | §32A | 3 calendar days after buyer signature |

| Earnest money deposited | §3D(1) | Within 3 business days of acceptance |

| Seller delivery of disclosures | §14A | Within 7 days of acceptance |

| Investigation contingency removal | §3L(3) / §8C | 17 days after acceptance |

| Appraisal contingency removal | §3L(2) / §8B | 17 days after acceptance |

| Loan contingency removal | §3L(1) / §8A | 17 days after acceptance |

| Final walkthrough | §16 | Within 5 days prior to COE |

| Default close of escrow | §3A | 30 days after acceptance |

Frequently Asked Questions

1. What happens if a buyer backs out of escrow in California?

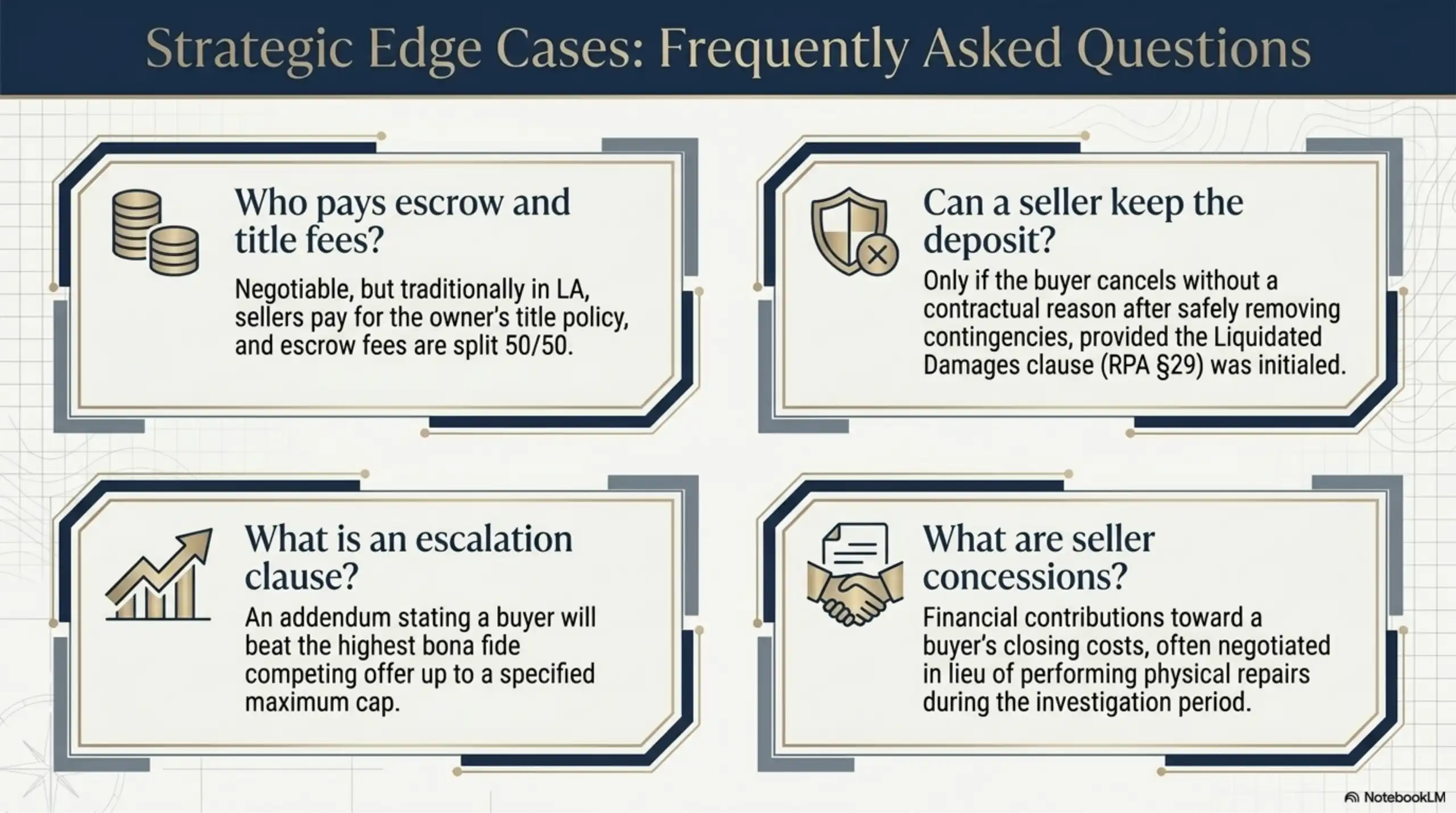

If a buyer cancels within an active contingency period, they receive a full refund of their earnest money deposit. If they cancel after all contingencies are removed without a contractual reason, the seller may retain the deposit if the Liquidated Damages clause is initialed.

2. What is the difference between escrow and title in California?

Escrow is the neutral third party managing the transaction, holding funds, and facilitating the close. Title refers to legal ownership, and title insurance protects against undiscovered claims. In SoCal, title and escrow are often handled together.

3. Can a seller keep a buyer’s deposit if the deal falls through?

Only if the buyer walks away after safely removing all contingencies without a valid contractual reason, and only if the Liquidated Damages clause was initialed by both parties.

4. What is a Notice to Buyer to Perform (NBP)?

A formal document a seller must issue giving the buyer a specific timeframe (usually 2 days) to remove contingencies or take a contractual action before the seller has the right to cancel the escrow.

5. Can I waive the appraisal contingency in Los Angeles?

Yes, and it is common in competitive bidding wars. However, if the home under-appraises, you are contractually obligated to bridge the gap between the appraised value and the purchase price in cash.

6. What are the current LA City transfer taxes including Measure ULA?

Standard LA City/County combined transfer tax is $5.60 per $1,000. Measure ULA adds 4% to properties sold over $5M, and 5.5% on properties over $10M within city limits.

7. How do interest rate fluctuations affect my escrow?

If rates jump during escrow and you haven’t locked your rate, it could alter your debt-to-income ratio, potentially threatening your loan approval.

8. What is the standard earnest money deposit (EMD) in LA?

The standard EMD is 3% of the agreed-upon purchase price, which is generally the maximum amount a seller can claim as liquidated damages in California.

9. What happens if a home appraises for less than the offer price?

If you have an appraisal contingency, you can request the seller lower the price, you can pay the difference in cash, or you can cancel the contract and retain your deposit.

10. How long does a seller have to respond to an offer?

By default in the California RPA, an offer expires 3 calendar days after the buyer signs it, unless a different timeframe is specified in the contract.

11. What is an escalation clause?

An addendum stating a buyer will pay a certain amount higher than the highest bona fide competing offer, up to a specified maximum cap.

12. Are termite inspections mandatory in California?

They are not legally mandatory statewide, but lenders may require them if signs of damage are noted by the appraiser. In LA, it is a highly recommended part of the buyer’s investigation.

13. What is a Request for Repair (RR)?

A formal form submitted by the buyer during their investigation contingency asking the seller to complete specific repairs or offer a closing cost credit in lieu of repairs.

14. What are seller concessions?

Financial contributions made by the seller toward the buyer’s closing costs, often negotiated in lieu of doing physical repairs to the property.

15. Who pays for escrow and title fees in Los Angeles?

This is negotiable. Traditionally in Los Angeles County, the seller pays for the owner’s title insurance policy, and escrow fees are split 50/50 between buyer and seller.

Ready to Start? Let’s Talk Strategy.

Whether you’re preparing to buy your first home in Greater Los Angeles or thinking about selling a luxury property you’ve held for years, the process is seamless when you have the right guidance from day one.

Request a Custom Equity Audit to see exactly what your property could command in today’s LA market.

Melissa Menard REALTOR® | Compass

Los Angeles & Surrounding Areas

📞 310.729.9726 | DRE# 01858710

📧 melissa@melissamenardhomes.com

🌐 www.MelissaMenardHomes.com

National Relocation Specialist

WSJ Real Trends Top 1% of Agents in America, 2022–2026

11601 Wilshire Boulevard, Suite 101, Los Angeles, CA 90025

Disclaimer: The information provided in this post is for educational purposes only and does not constitute financial, legal, or investment advice. Market conditions are subject to change. Please consult with a qualified professional regarding your specific real estate needs and local Fair Housing regulations.