For real estate investors across Southern California, internal revenue code Section 1031 is one of the most powerful wealth-building tools available. By allowing you to defer capital gains and depreciation recapture taxes when selling an investment property and reinvesting the proceeds into a “like-kind” replacement asset, it keeps 100% of your equity working for you.

However, the IRS does not hand out this benefit freely. The regulatory path is governed by rigid, unforgiving deadlines where being late by even a single minute can trigger an immediate, massive tax liability. In a hyper-competitive, high-velocity landscape like Los Angeles, understanding these timelines and holding rules is the difference between geometric wealth expansion and a devastating tax bill.

This deep dive breaks down the technical framework of 1031 exchange timing, reveals hidden traps like the “fourth-quarter tax return squeeze,” and outlines strategic execution paths tailored specifically for the L.A. luxury and commercial markets.

FAST FACTS

- Rigid Dual Countdown: The 1031 exchange timeline begins the day your relinquished property closes (Day 0). From that moment, two concurrent clocks start ticking: you have 45 calendar days to formally identify replacement properties and a total of 180 calendar days to close escrow on the replacement assets.

- The Tax Return Deadline Trap: Your absolute deadline to close on a replacement property is 180 days or the due date of your tax return for the year the sale occurred—whichever comes first. If you sell a property in the fourth quarter, your 1031 window is automatically shortened unless you file a federal tax extension.

- Strict “Constructive Receipt” Prohibitions: You cannot touch, hold, or direct the sales proceeds at any point during the transaction. All funds must flow through an independent Qualified Intermediary (QI) to preserve the tax shelter.

- Holding Rules & Intent: While the tax code doesn’t specify an exact minimum holding period to qualify for a 1031 exchange, IRS precedent strongly favors properties held for investment or business use for at least 12 to 24 months before exchanging.

The 1031 Exchange Clock: Understanding the Two Unforgiving Deadlines

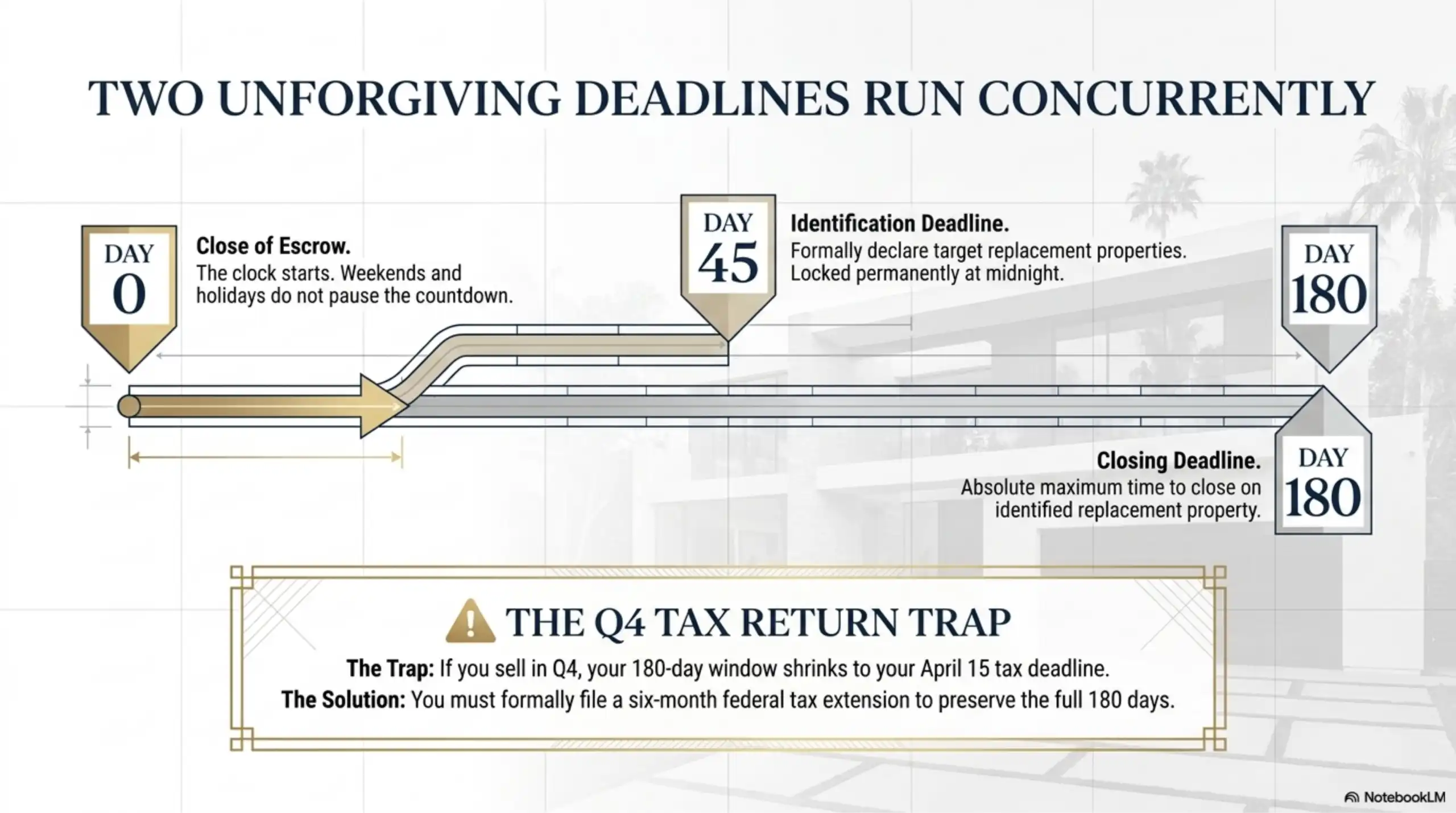

The moment title transfers on your sold (relinquished) property, the clock starts. The IRS measures these deadlines in strict calendar days, meaning weekends, federal holidays, and natural disruptions do not stop or pause the countdown.

1. The 45-Day Identification Period

You have exactly 45 days from the close of escrow to formally declare your intent to buy specific replacement properties.

- The Execution: The identification must be executed in writing, signed by you, and delivered to your Qualified Intermediary (QI) by midnight of the 45th day.

- Flexibility vs. Finality: Within those 45 days, you can amend, revoke, or substitute your list as often as market conditions dictate. However, on Day 46, your list is completely locked. If your identified properties fall through after Day 45, you cannot add a backup option; your exchange will fail, and the capital gains taxes will be due.

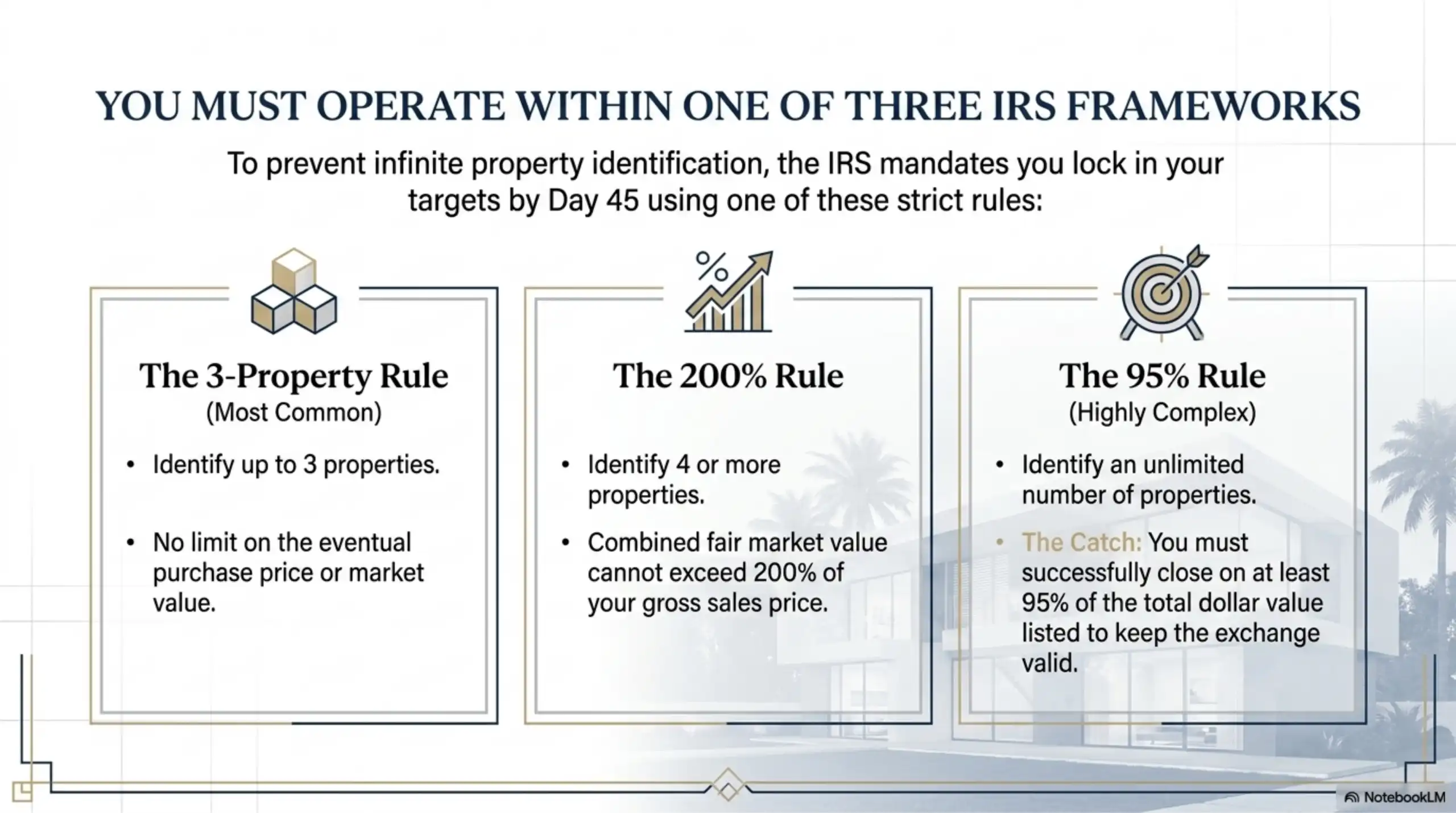

To protect investors from identifying an infinite number of properties, the IRS enforces three specific identification frameworks. You must operate within one of these rules:

- The Three-Property Rule: This is the most common path. You may identify up to three potential replacement properties of any market value, with no limit on the eventual purchase price.

- The 200% Rule: You can identify four or more properties, but their combined fair market value cannot exceed 200% of the gross sales price of the property you sold.

- The 95% Rule: You can identify an unlimited number of properties of any value, but the exchange only remains valid if you successfully close on at least 95% of the total dollar value of everything you listed. This rule is highly complex and rarely used by individual investors.

2. The 180-Day Exchange Period

You have a maximum of 180 calendar days from the sale of your relinquished property to close escrow on one or more of the assets listed on your 45-day identification form.

- Concurrent, Not Consecutive: A frequent misconception among investors is that you receive 45 days to identify, plus an additional 180 days to close (totaling 225 days). In reality, the two timelines run concurrently. The 180-day clock begins on Day 0, meaning you have exactly 135 days left to close once your identification window closes.

The Tax Return Deadline Trap: When 180 Days Shrinks

One of the most dangerous, overlooked clauses in Section 1031 is that the exchange period actually ends on the earlier of two dates:

- 180 days after the date the relinquished property is transferred.

- The due date (including extensions) of the taxpayer’s income tax return for the taxable year in which the relinquished property was sold.

If you close the sale of an investment property during the fourth quarter of the year, your 180-day window hits a wall on tax day of the following year.

For example, if an investor sells an apartment building in Santa Monica on December 1, the standard 180-day window would put their closing deadline at late May of the following year. However, because their individual federal tax return is due on April 15, the 1031 timeline is cut short by more than a month.

The Solution: To preserve the full 180-day window, the investor must formally file for a six-month federal tax extension before filing their tax return. This pushes the tax due date out to October, restoring the full 180 days to complete the property acquisition. Crucially, you must not file your final tax return until the 1031 exchange is fully completed and closed.

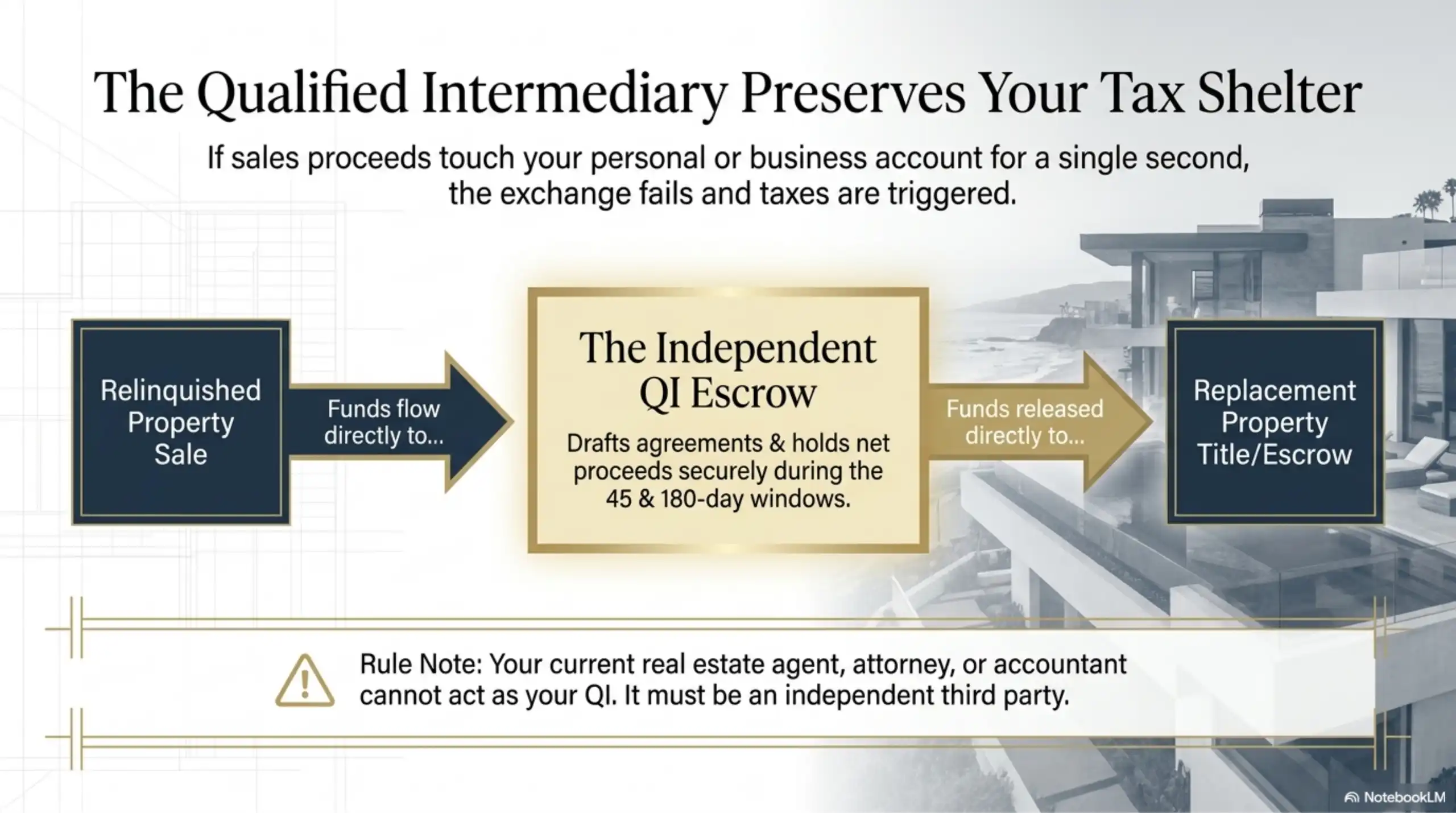

The Qualified Intermediary and Avoiding “Constructive Receipt”

To execute a legal 1031 exchange, you must completely avoid “constructive receipt” of the sales proceeds. If the capital from your sale touches your personal bank account, your escrow account, or is even held by an entity you control for a single second, the IRS deems that you have taken receipt of the profit, and the entire transaction becomes immediately taxable.

To prevent this, you must retain an independent Qualified Intermediary (QI) before closing the sale of your relinquished property.

[ Relinquished Property Sale ] ---> ( Sales Proceeds Sent Directly to QI Escrow )

|

v

[ Funds Held Securely During ]

[ 45-Day & 180-Day Windows ]

|

v

[ Replacement Property Purchase ] <--- ( QI Releases Funds Directly to Title/Escrow )

The QI acts as an essential legal buffer. They draft the exchange agreements, hold the net proceeds in a secure escrow account during the 45-day and 180-day windows, and then route those funds directly to the title company closing the purchase of your replacement property.

Deciphering “Holding Rules” and Investor Intent

A common question among property flippers and developers is: “How long do I need to hold a property before I can execute a 1031 exchange?”

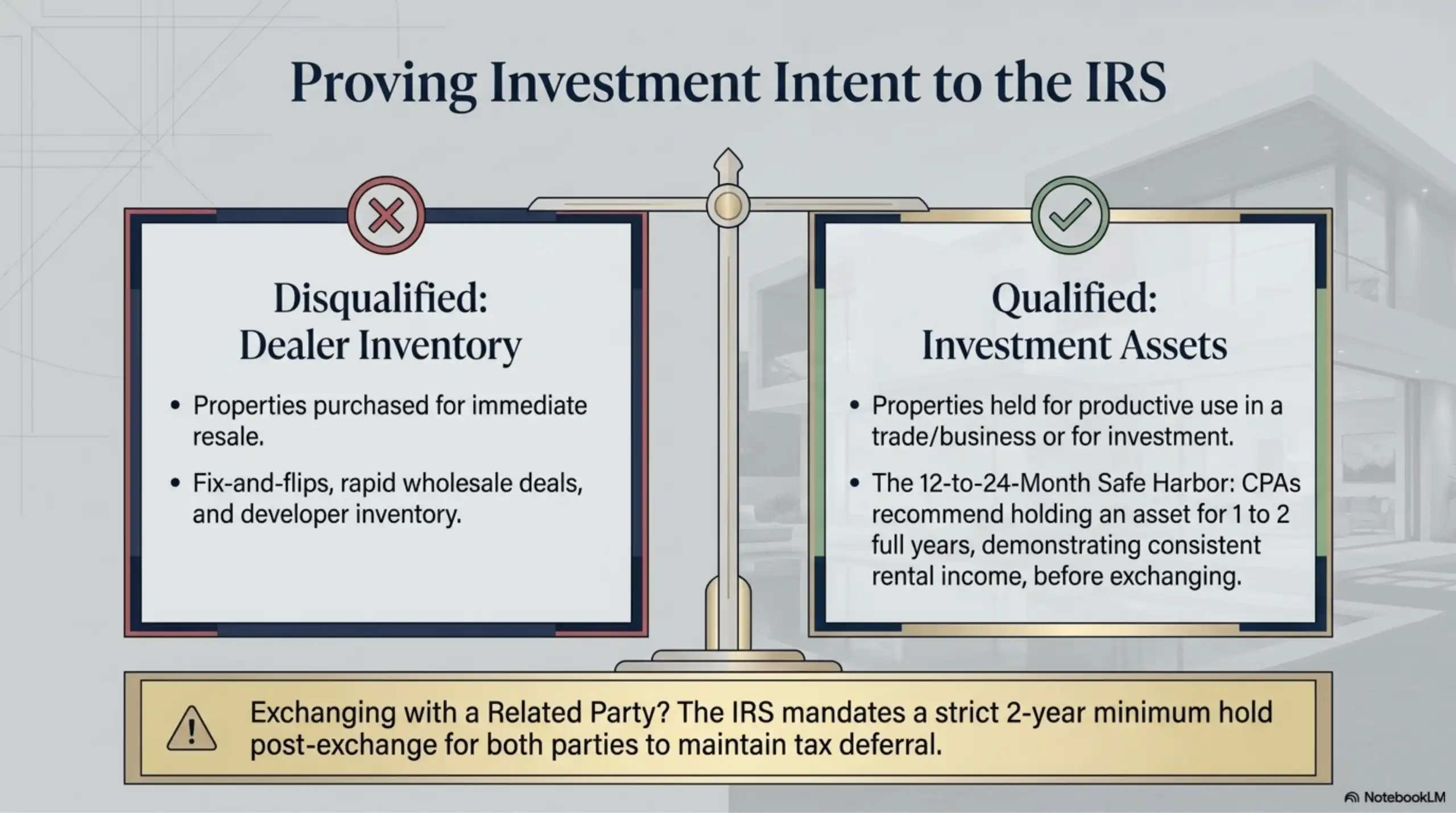

The text of IRC Section 1031 does not stipulate a mandatory minimum holding duration (e.g., 12 months or two years). Instead, the law focuses on intent. The statute states that both the property sold and the property acquired must be held for “productive use in a trade or business or for investment.”

Because of this focus on intent, properties purchased with the primary goal of immediate resale—such as fix-and-flips, rapid wholesale deals, or inventory built by developers—are explicitly disqualified from 1031 treatment. They are categorized as dealer inventory rather than investment assets.

Establishing Safe Harbor

While there is no codified timeline, historical IRS audits and tax court precedents have created a widely accepted benchmark:

- The 12-to-24-Month Rule of Thumb: Most tax attorneys and CPAs recommend holding an asset for a minimum of one to two full years, showing consistent rental income and investment treatment on your tax returns, before attempting a 1031 exchange.

- IRS Section 1031(f) for Related Parties: If you are exchanging properties with a related party (such as a family member or a controlled corporation), the tax code enforces a mandatory two-year minimum holding period post-exchange for both parties to maintain the tax deferral.

Navigating the 1031 Landscape in Los Angeles

Executing a flawless 1031 exchange requires hyper-localized strategy, particularly when dealing with the realities of the real estate market in Los Angeles and its surrounding coastal and metropolitan areas.

+-----------------------------------------------------------------------------+

| LOS ANGELES 1031 EXCHANGE STRATEGIES |

+-----------------------------------------------------------------------------+

| |

| [ INVENTORY CONSTRAINTS ] ----------------> [ STRATEGIC MITIGATION ] |

| * Low cap rates in Westside/Coastal * Source off-market assets |

| * Extreme competition on MLS * Leverage Compass private net |

| * 45-day window compression * Parallel escrow structures |

| |

| [ VALUATION BALANCING ] ------------------> [ EXECUTING THE FORMULA ] |

| * "Equal or Greater Value" rule * Target value-add multi-fam |

| * Must replicate or exceed debt * Transition to triple-net |

| * Avoid taxable "boot" leakage * NNN commercial options |

| |

+-----------------------------------------------------------------------------+

1. Countering High Competition and Thin Inventory

In premium Los Angeles submarkets—from luxury residential pockets in Beverly Hills and Malibu to high-density multifamily corridors in Santa Monica, Silver Lake, and Venice—available investment inventory is perpetually tight. Trying to source, underwrite, negotiate, and formally tie up a replacement property within a brief 45-day window is a high-stress endeavor.

To mitigate this risk, seasoned L.A. investors utilize a parallel tracking strategy. Do not wait until your relinquished property closes to start looking for its replacement. You should actively hunt for, tour, and underwrite target assets while your current property is still under contract. Ideally, you want to identify off-market opportunities or leverage private placement networks—such as the Compass private broker network—to secure a replacement property before your 45-day clock even begins.

2. Balancing the Debt and Equity Equation (Avoiding “Boot”)

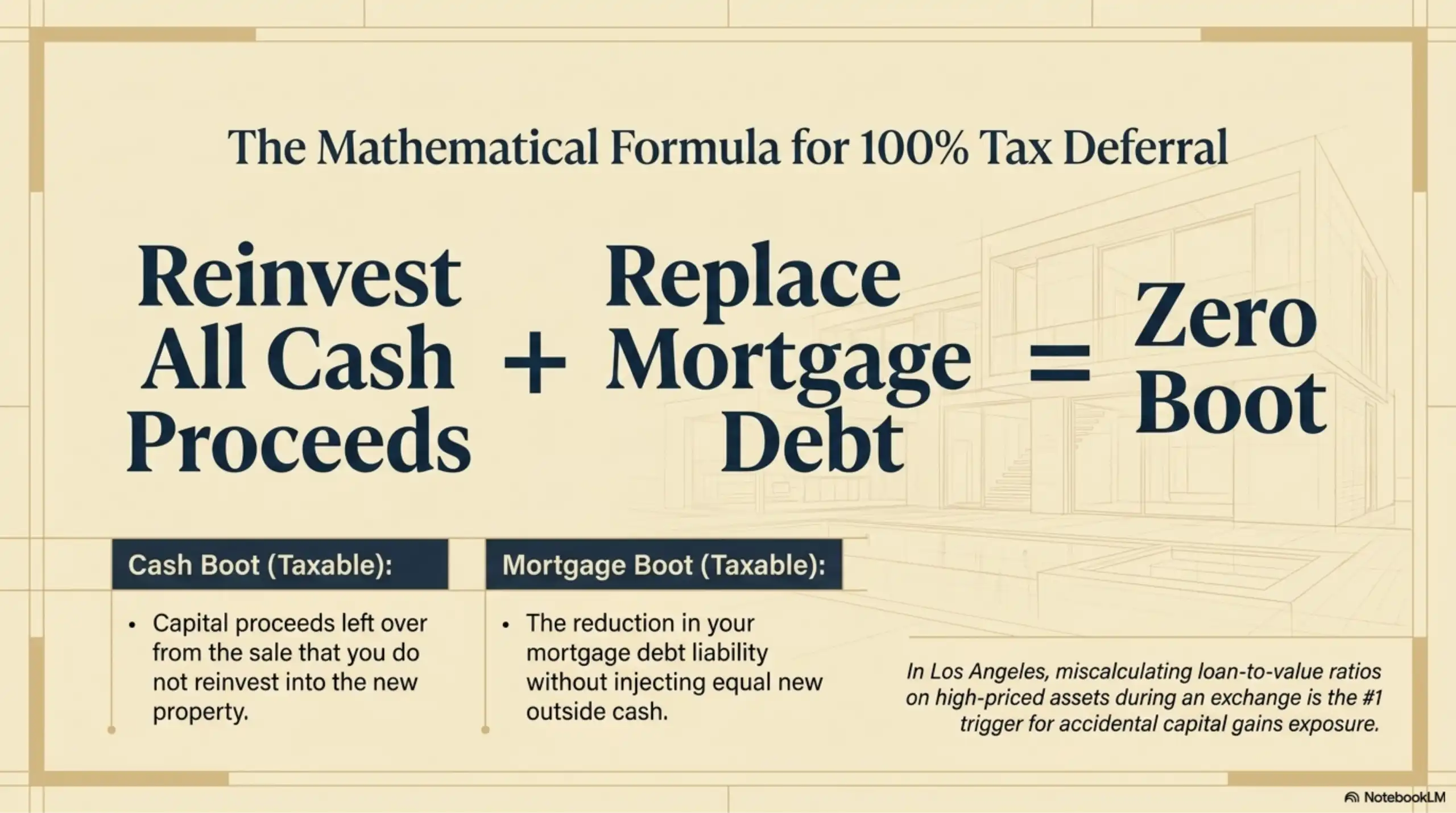

To achieve a completely tax-free exchange, you must adhere to the Equal or Greater Value Rule. This means your replacement property must have a net purchase price equal to or greater than the net sales price of the property you sold. Furthermore, you must reinvest all the cash proceeds and replace any existing mortgage debt on the old property with an equal or greater amount of debt on the new one.

If you trade down in value, or if you lower your mortgage liability without injecting an equal amount of cash, the difference is classified as “boot.”

- Cash Boot: Capital proceeds left over from the sale that you do not reinvest.

- Mortgage Boot (Debt Relief): The reduction in your mortgage debt liability.

In Los Angeles, where property values are significantly elevated, miscalculating loan-to-value ratios during an exchange frequently triggers accidental boot, resulting in unexpected, sizable capital gains exposures.

3. Transitioning Asset Classes: From Residential to Commercial NNN

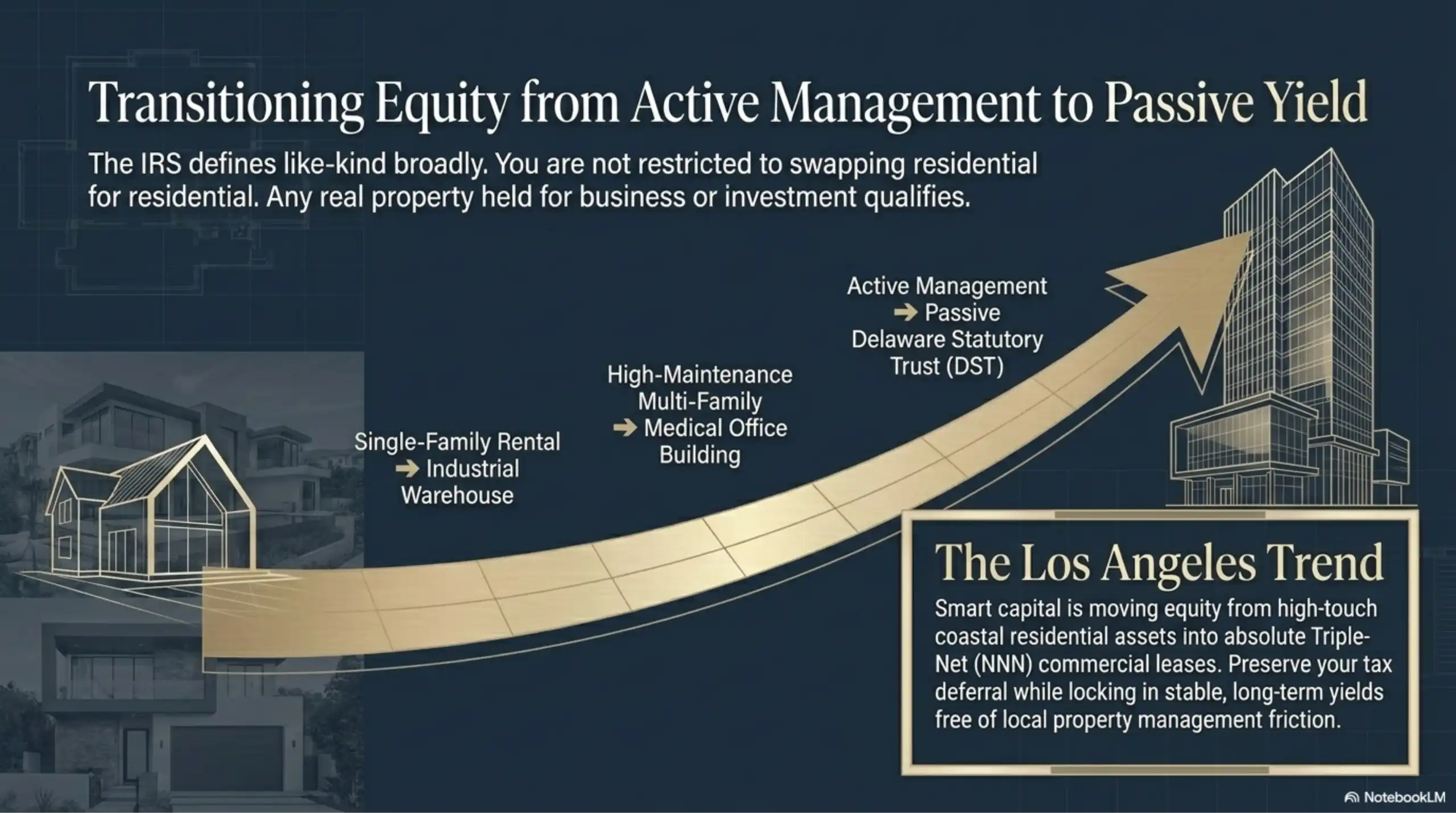

Many luxury property owners in Los Angeles are utilizing 1031 exchanges to transition away from high-maintenance residential properties into completely passive commercial assets.

Because the IRS defines “like-kind” incredibly broadly—essentially meaning any real property held for business or investment purposes—you can exchange a single-family rental property in Venice for an industrial warehouse in the Inland Empire, a medical office building in Pasadena, or a fractional share in a institutional-grade Delaware Statutory Trust (DST).

Moving equity from high-touch residential assets into absolute Triple-Net (NNN) commercial leases allows investors to preserve their tax deferral while locking in stable, long-term yields completely free of localized property management friction.

Frequently Asked Questions (FAQ’s)

1. What happens if I miss the 45-day identification deadline?

If midnight of the 45th day passes and you have not delivered a signed, written identification form listing valid replacement assets to your Qualified Intermediary, your exchange is immediately disqualified. Your QI will release the sales proceeds to you, and the entire transaction will be treated as a standard taxable sale, triggering capital gains and depreciation recapture taxes for that tax year.

2. Can I get an extension on the 45-day or 180-day deadlines?

No. The IRS is notoriously uncompromising regarding 1031 deadlines. Extensions are not granted for weekends, holidays, title delays, financing complications, or illness. The only exception is in the event of a presidentially declared disaster area, which may prompt a specific administrative extension for affected property owners.

3. Can I buy a more expensive replacement property than the one I sold?

Yes, absolutely. To achieve 100% tax deferral, buying a property of equal or greater value is required. If the replacement asset is more expensive, you simply cover the difference by procuring a larger mortgage, injecting new outside cash, or combining both methods.

4. What happens if I buy a less expensive replacement property?

If you purchase a replacement asset that is less expensive than your sold property, the exchange is considered a “partial exchange.” The transaction is still valid, but the difference in value (including any cash left over in the QI escrow or reduction in debt) will be classified as “boot” and will be subject to capital gains taxes.

5. Can I use a 1031 exchange on my primary residence?

No. Section 1031 applies strictly to properties held for productive use in a trade or business or for investment. Primary residences and personal-use vacation homes do not qualify. To minimize taxes on a primary residence, you must utilize the primary residence tax exclusion under IRC Section 121.

6. Can I convert a 1031 replacement property into my primary residence later?

Yes, but you must proceed with caution. To preserve the validity of the initial exchange, you must demonstrate clear intent that the asset was purchased as an investment. Safe harbor guidelines recommend renting the property out at fair market value for at least 14 days per year for two consecutive 12-month periods, while keeping your personal use under 14 days per year. If you later move in, you must live there for a minimum of five years before selling to utilize any Section 121 capital gains exclusions.

7. What types of real estate are considered “like-kind”?

The IRS interprets “like-kind” very broadly for real estate. Nearly all real property held for investment or business qualifies. You can exchange raw land for an apartment building, a retail storefront for an industrial warehouse, or a residential rental for a commercial office space. The physical layout of the property does not matter; its investment purpose does.

8. Who qualifies as a Qualified Intermediary (QI)?

A QI must be an independent third party. The tax code explicitly disqualifies anyone who has acted as your agent within the previous two years, which includes your current real estate agent, attorney, accountant, or escrow officer. Most reputable QIs are specialized institutional entities backed by substantial fidelity bonds and errors and omissions insurance.

9. Can I use the money from my 1031 sale to make renovations on the new property?

Yes, but only if the renovations are executed before you take legal title to the replacement property. This requires a highly specialized structure known as an Improvement Exchange or Construction Exchange, where an Exchange Accommodation Titleholder (EAT) takes title to the new asset, utilizes the exchange funds to complete the specified improvements, and then transfers the finished asset to you within the 180-day window.

10. What is “boot” in a 1031 exchange?

“Boot” is any non-like-kind property or asset received by the investor during an exchange. It most commonly takes the form of cash remaining in the QI escrow account after closing or “debt relief” (when your new mortgage is smaller than your old one). Boot is taxable up to the total amount of your realized capital gain.

11. Can I do a “Reverse Exchange” where I buy the new property first?

Yes. If a prime investment opportunity arises in Los Angeles but your current asset hasn’t sold yet, you can initiate a Reverse 1031 Exchange. In this scenario, an Exchange Accommodation Titleholder (EAT) parks and holds title to either your new replacement property or your current relinquished property. You then have the standard 180 calendar days to finalize the sale of your old property to complete the loop.

12. Are vacation rentals or Airbnb properties eligible for 1031 exchanges?

Yes, provided they meet the strict IRS safe harbor requirements under Revenue Procedure 2008-16. The property must be owned for at least 24 months prior to the exchange, and in each of those two 12-month periods, it must be rented out to third parties at a fair market rent for 14 days or more. Your personal use of the vacation rental cannot exceed the greater of 14 days or 10% of the total days it is actively rented.

13. How does depreciation recapture factor into a 1031 exchange?

When you sell a standard investment property, any structural depreciation you deducted over your ownership period is re-captured and taxed at a flat federal rate of up to 25%. A successful 1031 exchange fully defers this depreciation recapture tax along with your standard capital gains taxes, rolling that liability into the cost basis of the new asset.

14. Can I split the proceeds of a joint investment property into individual 1031 exchanges?

This depends entirely on how the property is titled. If the asset is owned by a partnership or an LLC, the entity itself must perform the 1031 exchange. Individual partners cannot split off independently. However, if the asset is held as Tenants in Common (TIC), each co-owner owns an undivided fractional interest in the real estate and has the right to independently execute a 1031 exchange with their specific share of the proceeds.

15. What happens if my identified replacement property falls through after Day 45?

If your identified properties fall through due to failed inspections, title defects, or financing rejections after Day 45, your exchange is effectively dead. You cannot add new properties to your selection form after the 45th day has passed. The exchange will fail, and your Qualified Intermediary will return your funds on Day 181, making the entire capital gain taxable for the year the original sale occurred.

Ready to Maximize Your Real Estate Portfolio?

Successfully executing a 1031 exchange in the competitive Los Angeles market requires advanced planning, a network of highly specialized tax experts, and immediate access to premium on- and off-market inventory. Whether you are seeking to transition from residential properties to passive commercial net-leases, or scaling up into high-yield multi-family assets, precision execution is paramount.

Request a Custom Equity Audit

Curious about what your current property is worth in today’s shifting market and how much capital you can defer? Contact me today for a tailored, data-backed portfolio equity analysis.

Melissa Menard REALTOR® | Compass

Los Angeles & Surrounding Areas

📞 310.729.9726 | DRE# 01858710

📧 melissa@melissamenardhomes.com

🌐 www.MelissaMenardHomes.com

Disclaimer: The information provided in this post is for educational purposes only and does not constitute financial, legal, or investment advice. Market conditions are subject to change. Please consult with a qualified professional, tax attorney, or CPA regarding your specific real estate needs and local Fair Housing regulations.